Alton Aviation Consultancy joint managing director Adam Cowburn argues travel bubbles could drive aviation’s resurgence, while his counterpart Jonathan Berger believes the maintenance and repair market is set to change.

Since the beginning of the pandemic, Covid-19 has decimated air travel demand, with statistics released by OAG’s Schedules Analyser showing the number of scheduled flights globally down by 52 per cent in the second week of July 2020, year on year.

As the virus spread, governments around the world imposed travel bans on specific countries which evolved into blanket border closures to curb inbound Covid-19 transmission from foreign visitors.

The result of these travel restrictions can be seen in declining revenue passenger kilometres (RPKs) and available seat kilometres (ASKs) since the end of 2019. Airlines responded to this reduced demand by cutting their capacity. Between January 2020 and May 2020, global ASKs declined by 45 per cent, with RPKs in May down 91 per cent and ASKs down by 86 per cent year on year.

Three-phase recovery

Economic and aviation experts have predicted a severe fall in both GDP and air traffic demand in 2020 as a result of Covid-19, constraining short-term air traffic growth. However, long-term air-traffic growth is expected broadly to follow projected pre-Covid trends with a three-phase recovery path.

The first, ongoing phase is deep crisis which will then lead to a period of recovery, albeit one with an overhang caused by Covid-19. The final phase of the process will be the establishment of a new normal.

In our white paper, Covid-19: Implications for the commercial aviation industry, we set out how the immediate phase of deep crisis for the aviation industry may come to an end in the not-too-distant future. Before settling into the new normal however, the industry will pass through an extended period featuring a Covid-19 overhang. While it remains unclear how long this period will last, we predict it will be at least 18 to 24 months until air travel settles into the new growth trajectory.

Weathering the Covid-19 overhang

Airlines have been fighting for survival for the last few months. As we approach the end of the deep crisis phase, airlines can now shift their focus from day-to-day crisis management to planning for both the immediate resumption of operations and the longer-term new normal.

Travel bubbles could provide a significant boost to demand and jump-start the resumption of operations for airlines. Travel bubbles enable people to fly internationally without the need to undergo lengthy quarantine periods upon arrival.

Successful implementation of these corridors has the potential to add 1.3 billion more seats into the air travel market, based on 2019 capacity data. This is equivalent to 44 per cent of domestic seat capacity, 54 per cent of international seat capacity and, collectively with domestic flights, represents 82 per cent of all airline seat capacity.

Airlines that primarily serve international routes or transit travel, especially those that have small or non-existent domestic markets including Singapore Airlines, Cathay Pacific or Middle Eastern carriers, would gain the most from these agreements.

However, even as international flight markets reopen within the travel bubbles, many passengers will be reluctant to fly while some businesses have curbed corporate travel.

Reducing ticket prices may be one way to stimulate demand, even if it means pushing yields lower – Chinese carriers adopted this approach when their domestic market reopened. A promise of superior health and safety standards could also be another way of assuring would-be passengers and stimulating airtravel demand.

Flight operations and frontline teams will need to be well staffed and well equipped to run airlines as smoothly as possible during this time. Until the markets stabilise, airlines should expect many irregularities as airports and governments constantly update immigration and health and safety rules, with some airports and borders potentially closing and reopening as the situation evolves.

Long-term planning in the new normal

As markets begin to reopen, network planning and scheduling teams will be as busy as ever. Processes that typically take weeks to complete must now speed up immeasurably. Planning difficulty has been compounded by very short booking horizons and the constant change in regulations and border restrictions thanks to Covid-19.

Use it or lose it slot rules have been widely suspended for the 2020 northern summer season. With slot alleviation for the winter season and beyond still uncertain, airlines must review their slot strategies now – they may no longer be able to afford non-profitable flights just to keep the slots in anticipation of recovering travel demand.

Based on the new network plans, airlines must decide which aircraft to bring back to service, which to retire or return and how to go about aircraft orders. They should use this time as an opportunity to simplify their fleets, reducing the variety of aircraft types and configurations. If this process is effectively done, airlines can lower their cost base significantly and better survive the immediate Covid-19 overhang.

While operating during the overhang, airlines must address the next level of strategic questions: how will demand change amid ongoing health concerns and the global shift in the corporate world to remote working? Should business models change and move away from targeting business traffic? What does it mean for fleets, networks, operations and cost bases in the long term? How do airlines weather another crisis?

Business-as-usual planning will not be enough. Airlines have to develop plausible recovery scenarios for the next 6, 12, 18 and 24 months, evaluating their financial stance and ability to survive in each of those time periods. In addition, they need a clear action plan for each scenario incorporating immediate action, strategic bets and a set of triggers to activate each action as the situation evolves.

Airlines will need to embrace agile decision making and adapt quickly in this rapidly changing environment as they discover that, in the new normal, traditional methods will no longer suffice.

The full report can be downloaded at altonaviation.com/news.

Engineering a new future

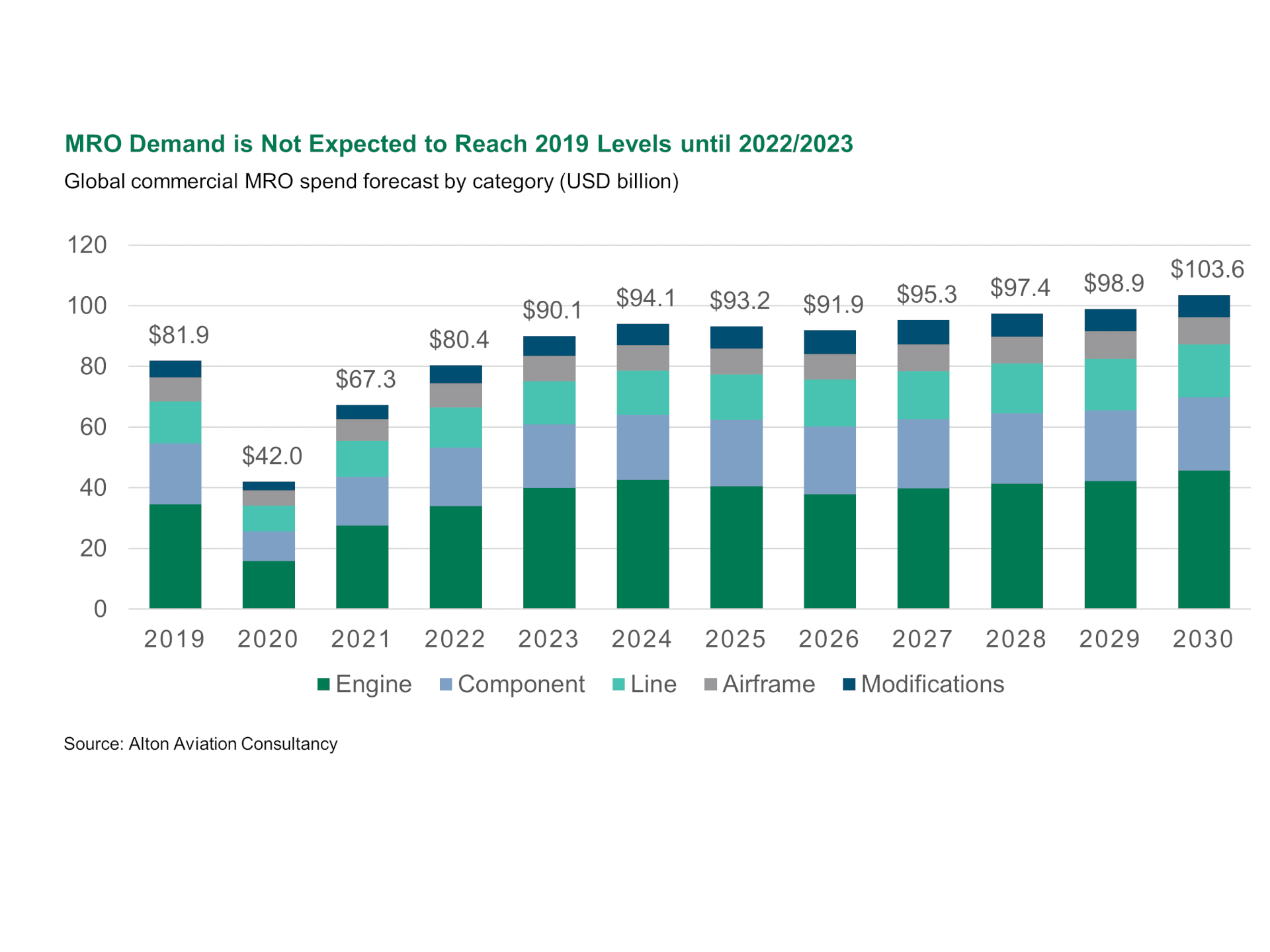

As of June 2020, approximately 63 per cent of the global passenger fleet remains grounded. According to Alton’s industry leading maintenance and repair organisation (MRO) demand model, which now incorporates the pandemic, this equates to an almost 50 per cent drop in MRO spend in 2020, down to $42 billion, with recovery to 2019 levels not expected until 2022-2023. However, there are still pockets of opportunities for MRO providers in this challenging environment.

Short-term opportunities with lessors include those that may have to re-possess aircraft and require lease-return or transition-check packages to ready aircraft for the next lessee. For airlines grounding aircraft, there are temporary storage maintenance activities required to keep aircraft airworthy should demand return faster than expected.

Further ahead, well-capitalised MRO suppliers could seek sale-leaseback opportunities for engines and aircraft components in order to enhance customers’ liquidity, while better positioning their businesses to capture post-pandemic, long-term MRO contracts. Additionally, airlines that have been performing certain MRO activities in house may now look to leverage this crisis as to convert more of their historically fixed MRO costs to variable via further outsourcing.

For MROs, the post-pandemic new normal will largely be defined by the aircraft models that make up of the majority of airline fleets over the coming decades. Older aircraft will see accelerated phase-out, while newer models will return to the skies after temporary storage. Knowing this, there are important considerations for MRO suppliers in the new normal.

First, define the key capability skill sets to retain and foster as pre-Covid-19 core capabilities may no longer apply. Second, define the desired strategy and business relationship with respect to original equipment manufacturers (OEMs) who will seek to play an ever-increasing role in the aftermarket. Full independence or full OEM alignment may not necessarily be mutually exclusive options.

Lastly, seek opportunistic mergers and acquisitions – there will continue to be industry consolidation, and for many MRO suppliers, this may ultimately be the right solution for post-Covid-19 survival.